Most international and cross-border sellers like me did suffer from creating a bank account in the buyer market. It’s in order to receive payments from global buyers. It can be because of high charging fees that eat out the profit, or back and forward admin and verification process. Or it’s because of even the waiting length for approval. However in the end the result might be a failure.

Likewise, locating the office in Hong Kong and running a global eCommerce company cannot move on without a business bank account as well. Particularly if you are running a small company or incorporated company, you should have probably heard of the challenges of setting up a bank account in Hong Kong for foreigners. Or even if you are a permanent HK resident, it’s very difficult to create a USA bank account to receive US Amazon selling business payments from buyers as well.

In this article, I will take the Hong Kong market as an example, and introduce HK B2B virtual bank options. These are what you should know and leverage to manage the international and cross-border payouts. By the end of this piece, you can understand the value of B2B virtual banks and the methodologies behind them. Also, you can select the most proper one for your cross-border business no matter if your business is located in HK, or other places worldwide.

- What’s a virtual bank?

- Traditional Bank vs Virtual Bank

- 5 B2B Virtual Bank Options for Cross Border Payments

- Verdict

What’s A Virtual Bank?

Virtual banks is a digital-only bank that has no physical base. For example in Hong Kong, these banks are registered as Hong Kong licensed banks. They are regulated under the HKMA and assured to maintain the safety standard as traditional banks. Virtual banks must follow certain banking provisions, KYC process, liquidity coverage, and capital requirements as well.

The virtual bank called Airwallex was founded less than six years in late 2015. It started out providing businesses with a cheaper, faster way to make cross-border payments. But also its services have expanded to include bank accounts, borderless cards (provided in partnership with Visa), online payments acceptance, and a suite of application programming interfaces. It also provides payment services for domestic transactions, as well as international ones. The latest capital raise increases the size of its Series D round to $US300 million, with US-based global investment firm Greenoaks coming on as the lead investor.

Virtual Bank vs Conventional Bank

Less Complexity and Less Admin Paperwork

Opening a bank account in Hong Kong requests your business some must-have documents. They are such as business registration issued by the Inland Revenue Department, representative’s HK IDs/passport, living/office address. It also needs to include a properly described declaration that provides the details of the principal shareholders and the directors, etc. And it might take you a long time of horrible verification. In the end, it might still fail due to non-sufficient documents. Even if you can successfully create a bank account, it doesn’t mean that you can create a payment collection bank account in the target market, such as the USA. It varies based on different country policies and then if it can. It requires you to provide more documents. It is a damn vicious cycle

For virtual bank account creation, on the other hand, we don’t need to prepare a complex list of documents. The virtual bank can require very fundamental documents, such as business registration, passport, office address. And also you can remotely create a virtual bank account instead of going to Hong Kong and having to sit there and wait. And you can finish the procedure for opening a business bank account with fintech options in no more than 2 weeks.

Then you can leverage the virtual bank feature to directly create a branch bank account to receive the payout from the global buyers. For example, the payout is from Amazon USA, Rakuten Japan, etc. That’s easy.

Multi-currency & Lower Transaction Commission

Basically, most virtual banks can allow you to receive payments from your buyers. Or you can pay suppliers in m. ulti-currencies, otherwise, you should not join that virtual bank without these. You get the real mid-market foreign exchange rate and eliminate correspondent bank fees with seamless cross-border payments. For the traditional bank, flexibility doesn’t exist basically.

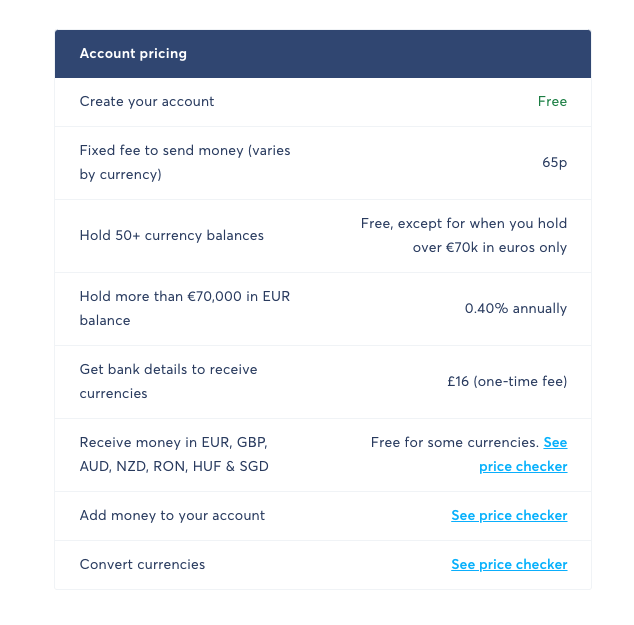

There are significant costs such as opening, maintaining, and closing traditional bank accounts. For many new and small businesses, these hefty fees aren’t always in reach. However, without the cost of physical branches, virtual banks normally offer lower fees, no minimums, and free account setup. The virtual bank only charges clients nominal transactional fees for payments. They also tend to offer more competitive foreign exchange rates, whereby clients can save up to more than traditional banks.

- Integration Capability with Online Payment Gateways and eCommerce Platforms

You might be suffering from headaches on how to create a US traditional bank account. It’s because you want to start your Amazon pro-seller business. It’s difficult if you are a newbie seller and don’t tend to invest too much at the very early stage of the business.

Virtual banks in fact do facilitate you create a bank account in the target market. And it also can integrate with the platforms. It definitely varies by different virtual banks, but this is a basic feature every virtual bank has.

Take Currenxie for an example. You create a virtual bank account in Hong Kong. Then you can work with Currenxie and integrate their collaborated business platforms to conveniently and easily receive your payouts from there.

Five B2B Virtual Bank Hong Kong Options for Collecting Cross Border Payments

Currenxie Virtual Bank

This virtual bank was founded in 2014 based in Hong Kong, and since 2014, it has grown to support up to 14 currencies per account. It allows business owners, who are based in Hong Kong, to create global bank accounts and get paid through the platform. It also offers personalized customer services to ensure you are fully informed before making any decisions.

It doesn’t charge any setup fee, monthly fee. And it currently supports the following currencies under its multi-currency account: AUD, CAD, CHF, CNH, DKK, EUR, GBP, HKD, JPY, NOK, NZD, SEK, SGD, USD. It normally takes up to 2 weeks for your account to get approved depending on what type of passport you are holding.

It uses mid-market exchange rates when converting between currencies. While it does not charge fees for receiving payments, it charges for foreign exchange conversion with a minimum fee of 25 USD for outgoing payments. Thus, Currenxie is better suited for larger payments.

Airwallex Virtual Bank

Airwallex supports business payments to over 130 countries. Its global financial infrastructure allows businesses have an easier way to set up global accounts. The accounts. support up to 14 currencies and that accept settlement via WeChat Pay as well.

It doesn’t charge any setup fee, monthly fee. Generally charging exchange rate margins are between 0.3% and 0.6% above interbank rates. Airwallex can help customers move money quickly and inexpensively around the world. Through Airwallex’s local payment technology, customers can send payments just like locals for free. Making a payment in non-local currencies attracts a SWIFT network fee. Also, when paying in Chinese Yuan, Airwallex charges an additional 0.1% payout fee.

Apart from main eCommerce platforms, businesses running on Xero accounting software can now link their Airwallex accounts with their respective accounting systems for ease of importing transactions.

Statrys Virtual Bank

Unlike some other operators, Statrys requires an opening fee and monthly fee from your account for some special companies. They are not incorporated in Hong Kong or Singapore, or those with special profiles. It supports 11 currencies, which include HKD, EUR, CNY, GBP, AUD, and more. It’s easily integrated into payment gateways like Paypal, Stripe, or Shopify, and also it has a debit master card service as well.

Having said that, the number of company jurisdictions that can register a Statrys business account is limited. Currently, accepted countries include Hong Kong, Singapore, and the BVI companies.

Neat Virtual Bank

Neat is a worth considering virtual bank in Hong Kong. With a Neat account, your assets are held in segregated bank accounts in licensed banks. It provides multiple currencies, such as HKD, USD, EUR, and so on. You can remotely create an account when you are not in Hong Kong. There is no initial deposit and maintenance fee. And they also provide prepaid master cards, visa cards. Last but not least, it’s easy to integrate with a payment gateway like Paypal, Stripe, or Amazon.

However, Neat as well as other conventional banks still apply certain requirements of acceptable nationalities and residing countries of applicants to open an account. Particularly, you are living in the list of serving countries. Or your directors/shareholders have residential addresses outside the list of serving countries, you would be rejected to open a Neat account.

The possibility of rejection can also be seen due to the business industry that your company is engaging in. You need to make sure that your business does not involve restricted industries. These sectors are from Neat like charities, finance, stock, and securities-related companies, gambling, and many others. Furthermore, the type of business may also impact the transfer limit of Hong Kong applicants.

TransferWise Virtual Bank

It must be a primary option in the spotlight for most p. eople. They would instantly mention it when talking about the virtual bank. This is all thanks to its international base and the real exchange rate.

It doesn’t charge fees on account creation, and it can provide multi-currency accounts with more than 50 currencies. They should be the most among alternatives. Also, it charges lower rates on currency exchange by using the real-time exchange rate. Outgoing money transfer fees are not low though.

One major disadvantage of using TransferWise maybe this. The account holders may be required to follow certain local regulations, depending on which place you have registered your account. For example, it is an e-money provider that is regulated by the Financial Conduct Authority in the UK. But, in Hong Kong, it is normally licensed as an MSO and regulated by the Customs and Excise Department of Hong Kong.

The spending limit for your card with TransferWise is another thing to mention. The limits may vary depending on different regions and countries. In addition, not all nationals can be eligible to register a TransferWise account. So it is a good tip that you should ask your service provider before determining whether it is the best fit solution for your business.

Verdict

Each business virtual bank has its unique selling point and stands out in Hong Kong for SMEs and incorporated companies. Having said that the common thing is the virtual bank account really speeds up the creation process. And it facilitates payment collection and sending in the operation process at a lower cost. As we know, profit margin might be impacted by higher costs from the conventional banks. No matter it’s the direct operational cost or opportunity cost

So easy, right? I hope you enjoy reading Leverage Business Virtual Banks to Receive Cross Border Payment from Buyers. If you did, please support us by doing one of the things listed below, because it always helps out our channel.

- Support my channel through PayPal (paypal.me/Easy2digital)

- Subscribe to my channel and turn on the notification bell Easy2Digital Youtube channel.

- Follow and like my page Easy2Digital Facebook page

- Share the article to your social network with the hashtag #easy2digital

- Buy products with Easy2Digital 10% OFF Discount code (Easy2DigitalNewBuyers2021)

- You sign up for our weekly newsletter to re. ceive Easy2Digital latest articles, videos, and discount code on Buyfromlo products and digital software

- Subscribe to our monthly membership through Patreon to enjoy exclusive benefits (www.patreon.com/louisludigital)